Noro's TrendMA StrategyThe strategy uses 2 moving averages. Fast and slow. SMA or EMA - the user can select. Moving averages are needed to identify the direction of the trend.

Trend

If both moving averages are directed upwards, it 's uptrend.

If both moving averages are pointing down, it 's downtrend.

If the moving averages are directed in different directions, the trend has not changed.

Background

Lime color is uptrend.

Red color is downtrend.

By default, background display is disabled, but you can enable it in script settings.

Trading

If uptrend (lime background) - open long position (and close short position)

If downtrend (red background) - open short position (and close long position)

Reverse trading, no stop-loss and take-profit

Short positions can be removed and only long positions can be traded.

For

- crypto/USD (XBT/USD, ETH/USD, etc)

- timeframes: 1h, 4h, 1d

ค้นหาในสคริปต์สำหรับ "the strat"

Hucklekiwi Pip - HLHB Trend-Catcher SystemThe strategy was authored by Hucklekiwi Pip back in 2015 and is still being updated today. She says that the system was designed to simply catch short-term forex trends. At its heart, the system is a simple EMA crossover strategy with a couple of other indicators used for confirming entries.

Strategy Rules

See her original post here:

www.babypips.com

Be sure to check out the updates and tweaks over the years!

HOW TO USE

For full information on how to use this strategy and how to correctly set the exit time, see this post:

backtest-rookies.com

Febres StrategyThe strategy consist in every time that price failed to break any of the EMAs, we need to wait for the right price action and make a buy or sell when it bounce from it to keep surfing on the trend (using the stochastic oscillator and the 5-13 EMAs cross as an additional confirmation).

When do we start looking for a change on the trend? When it repeats the blue tracer (high or low of the previous day) without breaking it and bouncing from it, there will be our signal to start looking for a change of direction on the trend.

Only applicable on 15 minute chart.

Sb_Rate_Of_Change_BB_Band_strategy Version 1.0The strategy couples the concept of rate of change along with the Bollinger bands.

Along with it LazyBear's RSI/MFI with Volatility Indicator is also taken to reduce the number of trades and improve efficiency.

Strategy (in Layman terms):

If in the past 10 candles RSI/MFI with Volatility Indicator has printed a red/green colour and the roc has gone above/below the Bollinger bands then the short/long order is placed respectively.

Message if you think of any modifications/ enhancements/ any opportunities. :)

Donations/Tips... :) -

BTC: 1BjswGcRR6c23pka7qh5t5k56j46cuyyy2

ETH: 0x64fed71c9d6c931639c7ba4671aeb6b05e6b3781

LTC: LKT2ykQ8QSzzfTDB6Tnsf12xwYPjgq95h4

SB_Compliment_RSI StrategyThe strategy modifies the original rsi strategy with the addition of compliment si (i.e. 100-rsi).

Strategy Idea: Previous rsi high and low value is recorded when the rsi crosses overBought(70) and OverSold(30) values.

Now when the rsi crosses above the overSold range, the rsi is matched with the compliment of previous high rsi value. If the compliment i.e.(100-prev_rsi_high) is less than or equal to rsi then long position is taken.

For short position, when the rsi crosses below the overBought range, the rsi is matched with the compliment of previous low rsi value. If compliment i.e.(100-prev_rsi_low) is greater than or equal to rsi.

Below s the code for the indicator present in the chart.

//@version=3

study(title="SB_Compliment_Relative Strength Index", shorttitle="RSI")

src = close, len = input(14, minval=1, title="Length")

up = rma(max(change(src), 0), len)

down = rma(-min(change(src), 0), len)

rsi = down == 0 ? 100 : up == 0 ? 0 : 100 - (100 / (1 + up / down))

plot(rsi, color=purple)

plot(100-rsi, color=orange)

band1 = hline(70)

band0 = hline(30)

fill(band1, band0, color=purple, transp=90)

The code also has switch code also which means it will enter the overBrought or overSold block one after the other.

Future modifications: Currently the value of rsi tracked is the one in which it crosses the overSold or OverBought range and not the highest/lowest value when the value is above/below OverBought/OverSold range.

Comment the perfect combination of indicators for it and will try to incorporate those indicators into it in the next version.

Message if you think of any modifications/ enhancements/ any opportunities. :)

Donations/Tips... :) -

BTC: 1BjswGcRR6c23pka7qh5t5k56j46cuyyy2

ETH: 0x64fed71c9d6c931639c7ba4671aeb6b05e6b3781

LTC: LKT2ykQ8QSzzfTDB6Tnsf12xwYPjgq95h4

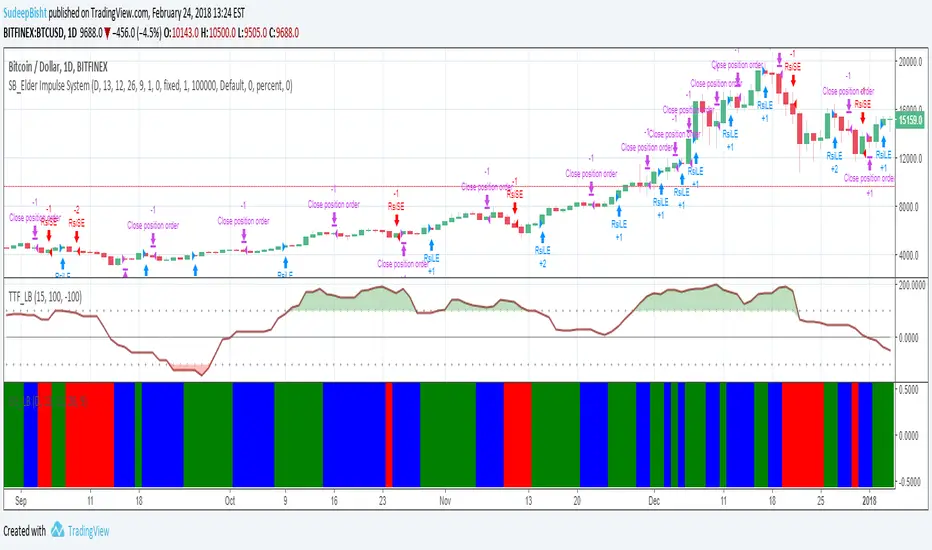

SB_Elder Impulse SystemThe strategy is based on LazyBear's Elder Impulse System

Strategy(in layman terms):

Long: When the green bar in the Elder Impulse System's indicator shows up

Short: When the red bar in the Elder Impulse System's indicator shows up

Close trade/Profit booking: When the blue bar in the Elder Impulse System's indicator shows up

Original Idea:

Message in the script if you think of any modifications/ enhancements.

Donations/Tips... :) -

BTC: 1BjswGcRR6c23pka7qh5t5k56j46cuyyy2

ETH: 0x64fed71c9d6c931639c7ba4671aeb6b05e6b3781

LTC: LKT2ykQ8QSzzfTDB6Tnsf12xwYPjgq95h4

Rainbow StrategyThe strategy is based on the following idea:

www.youtube.com

Not a fan of this but no script was present to show this idea's performance.

Best suitable for the 1-minute chart. You can change the ema values as per your needs.

For Tips to continue :) -

BTC: 1BjswGcRR6c23pka7qh5t5k56j46cuyyy2

ETH: 0x64fed71c9d6c931639c7ba4671aeb6b05e6b3781

LTC: LKT2ykQ8QSzzfTDB6Tnsf12xwYPjgq95h4

SB_CM_RSI_2_Strategy_Version 1.0The strategy is based on the indicator posted by @ChrisMoody "CM RSI-2 Strategy Lower Indicator" which is based on "Larry Connors RSI-2 Strategy - Lower RSI"

In this strategy the longs are placed when a green color is encountered in the rsi and short when red color is encountered in the rsi.

Although the profits can be booked at different interval.

Just message in the script if you have any different idea regarding this indicator.

For the original indicator you can refer to :

For Tips to continue :) :

BTC: 1BjswGcRR6c23pka7qh5t5k56j46cuyyy2

ETH: 0x64fed71c9d6c931639c7ba4671aeb6b05e6b3781

LTC: LKT2ykQ8QSzzfTDB6Tnsf12xwYPjgq95h4

Free Strategy #01 (ES / SPY)The strategy was designed to be traded based on daily data on the ES and SPY--the strategy was originally developed on NinjaTrader using approximately 50% out of sample data with a slippage of 1 tick on the ES. This is our first strategy that we converted from NinjaTrader to TradingView, so if you see any issues with our conversion, please let us know as we are still learning TradingView Pine Script.

Alerts v6The strategy includes:

✅ EMA-based trend direction (fast vs slow)

✅ RSI filtering for overbought/oversold control

✅ ADX confirmation for strong trend validation

✅ Pullback & BOS detection for precision entries

✅ Per-bar change logic for adaptive entry timing

✅ Session/day gating to control trading hours

✅ JSON alert integration for AI trading bots or webhooks

This script is Pine Script v6 compatible and optimized for automated alert-based trading setups such as AI trading bots, webhook systems, and VPS-linked executions.

Recommended Timeframes: 5m, 15m, 30m

Markets: XAUUSD, FX pairs, indices, and metals

CE+ZLSMA RovTrading StrateryThe strategy is optimized for scalping in small timeframes like M15 and M30, as well as M5.

It combines two indicators: CE and ZLSMA.

Try it now!

dabilThe strategy is probably to go short or long with the trend depending on the case, but if all time units 1 minute then 3 minutes then 5 minutes then 15 minutes then 1 hour all show the same direction, but first the 1 hour must be bullish in which the 1 hour candle closes above the previous one, for example if the trend is bearish then the market wants to change direction, then a 1 hour bullish close must then be followed by a 1 hour bearish close below the bullish candle, then another bullish candle must shoot above the previous bullish candle, then 15 minutes also shoot above the previous 15 bullish candles, then 1 and 2...3.5. Then I can rise with the market by only covering the last 15 bullish candles with my stop loss, if my SL is 50 pips then I want 100 pips and then I'm out.

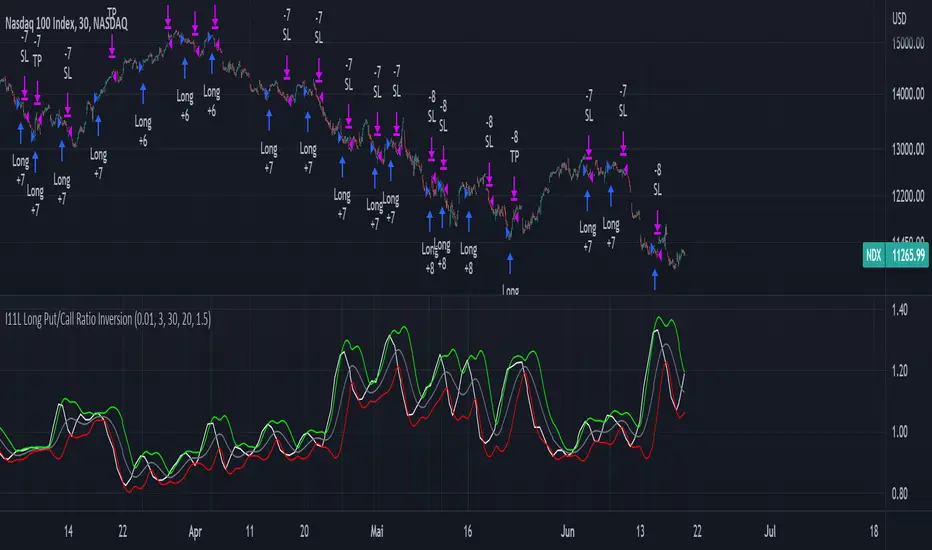

I11L Long Put/Call Ratio InversionThe Strategy uses the Put/Call Options Ratio Inversaion as a Signal and Implements simple Money Management rules.

It is adjusted for the NDX and for the SPX in the 30min Range.

The Oscilation has to be finetuned to reflect the correct Reversal point.

A good indicator of the correct Reversal Point is a solid range of good backtesting results..

The strategy example. Close position by timeoutThis is an example how to close open entries by timeout for educational purpose.

Trend Following or Mean RevertingThe strategy checks nature of the instruments. It Buys if the close is greater than yesterday's high, reverse the position if the close is lower than yesterday's low and repeat the process.

1. If it is trend following then the equity curve will be in uptrend

2. If it is mean reverting then the equity curve will be downtrend

Thanks to Rayner Teo.

Bollinger and Tendencies (Bollinger e Tendências )The strategy consists of buying when the price breaks up (crossover) the bottom line of the Bollinger and selling when the price breaks down (crossunder) to your top line.

The chart still shows trends clearly, with the fill between the exponential average and the closing value of the canlestick, green at high, red at low (this part of the script is based on the code: "Pivot Daily Price Color" by Rimko).

It also places notes on the high and low candlesticks (based on the code: "Candlesticks Pattern Identified" by Repo32).

It is recommended to use it in conjunction with the "IFR and Storage" script (also available to me), and some volume script.

A estratégia consiste em comprar quando o preço rompe para cima (crossover) a linha inferior do Bollinger e vender quando o preço rompe para baixo (crossunder) a sua linha superior.

O gráfico ainda mostra as tendências de forma clara, com o preenchimento entre a média exponencial e o valor de fechamento do canlestick, verde em alta, vermelho em baixa (essa parte do script é baseada no código: "Pivot Daily Price Color" do usuário: Rimko).

Também, coloca apontamentos nos candlesticks de alta e de baixa (baseado no código: "Candlesticks Pattern Identified" do usuário Repo32).

Recomenda-se a utilização em conjunto com o script "IFR e Estocagem" (também por mim disponibilizado), e algum script de volume.

SB_Volume_oscillator_Prev_high_lowThe strategy is a take on traditional volume oscillator.

In Layman terms:

The script places an order when the oscillator crosses the zero mark in the volume oscillator.

If the previous high is greater than the absolute value of previous low then a long order is placed

And if the absolute previous low is greater than the previous high then a shrt order is placed.

Last script (bandwidth focus on other monetary works. If you have any opportunities ping me)

Message if you think of any modifications/ enhancements/ any opportunities. :)

Donations/Tips... :) -

BTC: 1BjswGcRR6c23pka7qh5t5k56j46cuyyy2

ETH: 0x64fed71c9d6c931639c7ba4671aeb6b05e6b3781

LTC: LKT2ykQ8QSzzfTDB6Tnsf12xwYPjgq95h4

TRADINGLibrary "TRADING"

This library is a client script for making a webhook signal formatted string to PoABOT server.

entry_message(password, percent, leverage, margin_mode, kis_number)

Create a entry message for POABOT

Parameters:

password (string) : (string) The password of your bot.

percent (float) : (float) The percent for entry based on your wallet balance.

leverage (int) : (int) The leverage of entry. If not set, your levereage doesn't change.

margin_mode (string) : (string) The margin mode for trade(only for OKX). "cross" or "isolated"

kis_number (int) : (int) The number of koreainvestment account. Default 1

Returns: (string) A json formatted string for webhook message.

order_message(password, percent, leverage, margin_mode, kis_number)

Create a order message for POABOT

Parameters:

password (string) : (string) The password of your bot.

percent (float) : (float) The percent for entry based on your wallet balance.

leverage (int) : (int) The leverage of entry. If not set, your levereage doesn't change.

margin_mode (string) : (string) The margin mode for trade(only for OKX). "cross" or "isolated"

kis_number (int) : (int) The number of koreainvestment account. Default 1

Returns: (string) A json formatted string for webhook message.

close_message(password, percent, margin_mode, kis_number)

Create a close message for POABOT

Parameters:

password (string) : (string) The password of your bot.

percent (float) : (float) The percent for close based on your wallet balance.

margin_mode (string) : (string) The margin mode for trade(only for OKX). "cross" or "isolated"

kis_number (int) : (int) The number of koreainvestment account. Default 1

Returns: (string) A json formatted string for webhook message.

exit_message(password, percent, margin_mode, kis_number)

Create a exit message for POABOT

Parameters:

password (string) : (string) The password of your bot.

percent (float) : (float) The percent for exit based on your wallet balance.

margin_mode (string) : (string) The margin mode for trade(only for OKX). "cross" or "isolated"

kis_number (int) : (int) The number of koreainvestment account. Default 1

Returns: (string) A json formatted string for webhook message.

manual_message(password, exchange, base, quote, side, qty, price, percent, leverage, margin_mode, kis_number, order_name)

Create a manual message for POABOT

Parameters:

password (string) : (string) The password of your bot.

exchange (string) : (string) The exchange

base (string) : (string) The base

quote (string) : (string) The quote of order message

side (string) : (string) The side of order messsage

qty (float) : (float) The qty of order message

price (float) : (float) The price of order message

percent (float) : (float) The percent for order based on your wallet balance.

leverage (int) : (int) The leverage of entry. If not set, your levereage doesn't change.

margin_mode (string) : (string) The margin mode for trade(only for OKX). "cross" or "isolated"

kis_number (int) : (int) The number of koreainvestment account.

order_name (string) : (string) The name of order message

Returns: (string) A json formatted string for webhook message.

in_trade(start_time, end_time, hide_trade_line)

Create a trade start line

Parameters:

start_time (int) : (int) The start of time.

end_time (int) : (int) The end of time.

hide_trade_line (bool) : (bool) if true, hide trade line. Default false.

Returns: (bool) Get bool for trade based on time range.

real_qty(qty, precision, leverage, contract_size, default_qty_type, default_qty_value)

Get exchange specific real qty

Parameters:

qty (float) : (float) qty

precision (float) : (float) precision

leverage (int) : (int) leverage

contract_size (float) : (float) contract_size

default_qty_type (string)

default_qty_value (float)

Returns: (float) exchange specific qty.

method set(this, password, start_time, end_time, leverage, initial_capital, default_qty_type, default_qty_value, margin_mode, contract_size, kis_number, entry_percent, close_percent, exit_percent, fixed_qty, fixed_cash, real, auto_alert_message, hide_trade_line)

Set bot object.

Namespace types: bot

Parameters:

this (bot)

password (string) : (string) password for poabot.

start_time (int) : (int) start_time timestamp.

end_time (int) : (int) end_time timestamp.

leverage (int) : (int) leverage.

initial_capital (float)

default_qty_type (string)

default_qty_value (float)

margin_mode (string) : (string) The margin mode for trade(only for OKX). "cross" or "isolated"

contract_size (float)

kis_number (int) : (int) kis_number for poabot.

entry_percent (float) : (float) entry_percent for poabot.

close_percent (float) : (float) close_percent for poabot.

exit_percent (float) : (float) exit_percent for poabot.

fixed_qty (float) : (float) fixed qty.

fixed_cash (float) : (float) fixed cash.

real (bool) : (bool) convert qty for exchange specific.

auto_alert_message (bool) : (bool) convert alert_message for exchange specific.

hide_trade_line (bool) : (bool) if true, Hide trade line. Default false.

Returns: (void)

method print(this, message)

Print message using log table.

Namespace types: bot

Parameters:

this (bot)

message (string)

Returns: (void)

method start_trade(this)

start trade using start_time and end_time

Namespace types: bot

Parameters:

this (bot)

Returns: (void)

method entry(this, id, direction, qty, limit, stop, oca_name, oca_type, comment, alert_message, when)

It is a command to enter market position. If an order with the same ID is already pending, it is possible to modify the order. If there is no order with the specified ID, a new order is placed. To deactivate an entry order, the command strategy.cancel or strategy.cancel_all should be used. In comparison to the function strategy.order, the function strategy.entry is affected by pyramiding and it can reverse market position correctly. If both 'limit' and 'stop' parameters are 'NaN', the order type is market order.

Namespace types: bot

Parameters:

this (bot)

id (string) : (string) A required parameter. The order identifier. It is possible to cancel or modify an order by referencing its identifier.

direction (string) : (string) A required parameter. Market position direction: 'strategy.long' is for long, 'strategy.short' is for short.

qty (float) : (float) An optional parameter. Number of contracts/shares/lots/units to trade. The default value is 'NaN'.

limit (float) : (float) An optional parameter. Limit price of the order. If it is specified, the order type is either 'limit', or 'stop-limit'. 'NaN' should be specified for any other order type.

stop (float) : (float) An optional parameter. Stop price of the order. If it is specified, the order type is either 'stop', or 'stop-limit'. 'NaN' should be specified for any other order type.

oca_name (string) : (string) An optional parameter. Name of the OCA group the order belongs to. If the order should not belong to any particular OCA group, there should be an empty string.

oca_type (string) : (string) An optional parameter. Type of the OCA group. The allowed values are: "strategy.oca.none" - the order should not belong to any particular OCA group; "strategy.oca.cancel" - the order should belong to an OCA group, where as soon as an order is filled, all other orders of the same group are cancelled; "strategy.oca.reduce" - the order should belong to an OCA group, where if X number of contracts of an order is filled, number of contracts for each other order of the same OCA group is decreased by X.

comment (string) : (string) An optional parameter. Additional notes on the order.

alert_message (string) : (string) An optional parameter which replaces the {{strategy.order.alert_message}} placeholder when it is used in the "Create Alert" dialog box's "Message" field.

when (bool) : (bool) An optional parmeter. Condition, deprecated.

Returns: (void)

method order(this, id, direction, qty, limit, stop, oca_name, oca_type, comment, alert_message, when)

It is a command to place order. If an order with the same ID is already pending, it is possible to modify the order. If there is no order with the specified ID, a new order is placed. To deactivate order, the command strategy.cancel or strategy.cancel_all should be used. In comparison to the function strategy.entry, the function strategy.order is not affected by pyramiding. If both 'limit' and 'stop' parameters are 'NaN', the order type is market order.

Namespace types: bot

Parameters:

this (bot)

id (string) : (string) A required parameter. The order identifier. It is possible to cancel or modify an order by referencing its identifier.

direction (string) : (string) A required parameter. Market position direction: 'strategy.long' is for long, 'strategy.short' is for short.

qty (float) : (float) An optional parameter. Number of contracts/shares/lots/units to trade. The default value is 'NaN'.

limit (float) : (float) An optional parameter. Limit price of the order. If it is specified, the order type is either 'limit', or 'stop-limit'. 'NaN' should be specified for any other order type.

stop (float) : (float) An optional parameter. Stop price of the order. If it is specified, the order type is either 'stop', or 'stop-limit'. 'NaN' should be specified for any other order type.

oca_name (string) : (string) An optional parameter. Name of the OCA group the order belongs to. If the order should not belong to any particular OCA group, there should be an empty string.

oca_type (string) : (string) An optional parameter. Type of the OCA group. The allowed values are: "strategy.oca.none" - the order should not belong to any particular OCA group; "strategy.oca.cancel" - the order should belong to an OCA group, where as soon as an order is filled, all other orders of the same group are cancelled; "strategy.oca.reduce" - the order should belong to an OCA group, where if X number of contracts of an order is filled, number of contracts for each other order of the same OCA group is decreased by X.

comment (string) : (string) An optional parameter. Additional notes on the order.

alert_message (string) : (string) An optional parameter which replaces the {{strategy.order.alert_message}} placeholder when it is used in the "Create Alert" dialog box's "Message" field.

when (bool) : (bool) An optional parmeter. Condition, deprecated.

Returns: (void)

method close_all(this, comment, alert_message, immediately, when)

Exits the current market position, making it flat.

Namespace types: bot

Parameters:

this (bot)

comment (string) : (string) An optional parameter. Additional notes on the order.

alert_message (string) : (string) An optional parameter which replaces the {{strategy.order.alert_message}} placeholder when it is used in the "Create Alert" dialog box's "Message" field.

immediately (bool) : (bool) An optional parameter. If true, the closing order will be executed on the tick where it has been placed, ignoring the strategy parameters that restrict the order execution to the open of the next bar. The default is false.

when (bool) : (bool) An optional parmeter. Condition, deprecated.

Returns: (void)

method cancel(this, id, when)

It is a command to cancel/deactivate pending orders by referencing their names, which were generated by the functions: strategy.order, strategy.entry and strategy.exit.

Namespace types: bot

Parameters:

this (bot)

id (string) : (string) A required parameter. The order identifier. It is possible to cancel an order by referencing its identifier.

when (bool) : (bool) An optional parmeter. Condition, deprecated.

Returns: (void)

method cancel_all(this, when)

It is a command to cancel/deactivate all pending orders, which were generated by the functions: strategy.order, strategy.entry and strategy.exit.

Namespace types: bot

Parameters:

this (bot)

when (bool) : (bool) An optional parmeter. Condition, deprecated.

Returns: (void)

method close(this, id, comment, qty, qty_percent, alert_message, immediately, when)

It is a command to exit from the entry with the specified ID. If there were multiple entry orders with the same ID, all of them are exited at once. If there are no open entries with the specified ID by the moment the command is triggered, the command will not come into effect. The command uses market order. Every entry is closed by a separate market order.

Namespace types: bot

Parameters:

this (bot)

id (string) : (string) A required parameter. The order identifier. It is possible to close an order by referencing its identifier.

comment (string) : (string) An optional parameter. Additional notes on the order.

qty (float) : (float) An optional parameter. Number of contracts/shares/lots/units to exit a trade with. The default value is 'NaN'.

qty_percent (float) : (float) Defines the percentage (0-100) of the position to close. Its priority is lower than that of the 'qty' parameter. Optional. The default is 100.

alert_message (string) : (string) An optional parameter which replaces the {{strategy.order.alert_message}} placeholder when it is used in the "Create Alert" dialog box's "Message" field.

immediately (bool) : (bool) An optional parameter. If true, the closing order will be executed on the tick where it has been placed, ignoring the strategy parameters that restrict the order execution to the open of the next bar. The default is false.

when (bool) : (bool) An optional parmeter. Condition, deprecated.

Returns: (void)

ticks_to_price(ticks, from)

Converts ticks to a price offset from the supplied price or the average entry price.

Parameters:

ticks (float) : (float) Ticks to convert to a price.

from (float) : (float) A price that can be used to calculate from. Optional. The default value is `strategy.position_avg_price`.

Returns: (float) A price level that has a distance from the entry price equal to the specified number of ticks.

method exit(this, id, from_entry, qty, qty_percent, profit, limit, loss, stop, trail_price, trail_points, trail_offset, oca_name, comment, comment_profit, comment_loss, comment_trailing, alert_message, alert_profit, alert_loss, alert_trailing, when)

It is a command to exit either a specific entry, or whole market position. If an order with the same ID is already pending, it is possible to modify the order. If an entry order was not filled, but an exit order is generated, the exit order will wait till entry order is filled and then the exit order is placed. To deactivate an exit order, the command strategy.cancel or strategy.cancel_all should be used. If the function strategy.exit is called once, it exits a position only once. If you want to exit multiple times, the command strategy.exit should be called multiple times. If you use a stop loss and a trailing stop, their order type is 'stop', so only one of them is placed (the one that is supposed to be filled first). If all the following parameters 'profit', 'limit', 'loss', 'stop', 'trail_points', 'trail_offset' are 'NaN', the command will fail. To use market order to exit, the command strategy.close or strategy.close_all should be used.

Namespace types: bot

Parameters:

this (bot)

id (string) : (string) A required parameter. The order identifier. It is possible to cancel or modify an order by referencing its identifier.

from_entry (string) : (string) An optional parameter. The identifier of a specific entry order to exit from it. To exit all entries an empty string should be used. The default values is empty string.

qty (float) : (float) An optional parameter. Number of contracts/shares/lots/units to exit a trade with. The default value is 'NaN'.

qty_percent (float) : (float) Defines the percentage of (0-100) the position to close. Its priority is lower than that of the 'qty' parameter. Optional. The default is 100.

profit (float) : (float) An optional parameter. Profit target (specified in ticks). If it is specified, a limit order is placed to exit market position when the specified amount of profit (in ticks) is reached. The default value is 'NaN'.

limit (float) : (float) An optional parameter. Profit target (requires a specific price). If it is specified, a limit order is placed to exit market position at the specified price (or better). Priority of the parameter 'limit' is higher than priority of the parameter 'profit' ('limit' is used instead of 'profit', if its value is not 'NaN'). The default value is 'NaN'.

loss (float) : (float) An optional parameter. Stop loss (specified in ticks). If it is specified, a stop order is placed to exit market position when the specified amount of loss (in ticks) is reached. The default value is 'NaN'.

stop (float) : (float) An optional parameter. Stop loss (requires a specific price). If it is specified, a stop order is placed to exit market position at the specified price (or worse). Priority of the parameter 'stop' is higher than priority of the parameter 'loss' ('stop' is used instead of 'loss', if its value is not 'NaN'). The default value is 'NaN'.

trail_price (float) : (float) An optional parameter. Trailing stop activation level (requires a specific price). If it is specified, a trailing stop order will be placed when the specified price level is reached. The offset (in ticks) to determine initial price of the trailing stop order is specified in the 'trail_offset' parameter: X ticks lower than activation level to exit long position; X ticks higher than activation level to exit short position. The default value is 'NaN'.

trail_points (float) : (float) An optional parameter. Trailing stop activation level (profit specified in ticks). If it is specified, a trailing stop order will be placed when the calculated price level (specified amount of profit) is reached. The offset (in ticks) to determine initial price of the trailing stop order is specified in the 'trail_offset' parameter: X ticks lower than activation level to exit long position; X ticks higher than activation level to exit short position. The default value is 'NaN'.

trail_offset (float) : (float) An optional parameter. Trailing stop price (specified in ticks). The offset in ticks to determine initial price of the trailing stop order: X ticks lower than 'trail_price' or 'trail_points' to exit long position; X ticks higher than 'trail_price' or 'trail_points' to exit short position. The default value is 'NaN'.

oca_name (string) : (string) An optional parameter. Name of the OCA group (oca_type = strategy.oca.reduce) the profit target, the stop loss / the trailing stop orders belong to. If the name is not specified, it will be generated automatically.

comment (string) : (string) Additional notes on the order. If specified, displays near the order marker on the chart. Optional. The default is na.

comment_profit (string) : (string) Additional notes on the order if the exit was triggered by crossing `profit` or `limit` specifically. If specified, supercedes the `comment` parameter and displays near the order marker on the chart. Optional. The default is na.

comment_loss (string) : (string) Additional notes on the order if the exit was triggered by crossing `stop` or `loss` specifically. If specified, supercedes the `comment` parameter and displays near the order marker on the chart. Optional. The default is na.

comment_trailing (string) : (string) Additional notes on the order if the exit was triggered by crossing `trail_offset` specifically. If specified, supercedes the `comment` parameter and displays near the order marker on the chart. Optional. The default is na.

alert_message (string) : (string) Text that will replace the '{{strategy.order.alert_message}}' placeholder when one is used in the "Message" field of the "Create Alert" dialog. Optional. The default is na.

alert_profit (string) : (string) Text that will replace the '{{strategy.order.alert_message}}' placeholder when one is used in the "Message" field of the "Create Alert" dialog. Only replaces the text if the exit was triggered by crossing `profit` or `limit` specifically. Optional. The default is na.

alert_loss (string) : (string) Text that will replace the '{{strategy.order.alert_message}}' placeholder when one is used in the "Message" field of the "Create Alert" dialog. Only replaces the text if the exit was triggered by crossing `stop` or `loss` specifically. Optional. The default is na.

alert_trailing (string) : (string) Text that will replace the '{{strategy.order.alert_message}}' placeholder when one is used in the "Message" field of the "Create Alert" dialog. Only replaces the text if the exit was triggered by crossing `trail_offset` specifically. Optional. The default is na.

when (bool) : (bool) An optional parmeter. Condition, deprecated.

Returns: (void)

percent_to_ticks(percent, from)

Converts a percentage of the supplied price or the average entry price to ticks.

Parameters:

percent (float) : (float) The percentage of supplied price to convert to ticks. 50 is 50% of the entry price.

from (float) : (float) A price that can be used to calculate from. Optional. The default value is `strategy.position_avg_price`.

Returns: (float) A value in ticks.

percent_to_price(percent, from)

Converts a percentage of the supplied price or the average entry price to a price.

Parameters:

percent (float) : (float) The percentage of the supplied price to convert to price. 50 is 50% of the supplied price.

from (float) : (float) A price that can be used to calculate from. Optional. The default value is `strategy.position_avg_price`.

Returns: (float) A value in the symbol's quote currency (USD for BTCUSD).

bot

Fields:

password (series__string)

start_time (series__integer)

end_time (series__integer)

leverage (series__integer)

initial_capital (series__float)

default_qty_type (series__string)

default_qty_value (series__float)

margin_mode (series__string)

contract_size (series__float)

kis_number (series__integer)

entry_percent (series__float)

close_percent (series__float)

exit_percent (series__float)

log_table (series__table)

fixed_qty (series__float)

fixed_cash (series__float)

real (series__bool)

auto_alert_message (series__bool)

hide_trade_line (series__bool)

HYE Combo Market [Strategy] (Vwap Mean Reversion + Trend Hunter)In this strategy, I used a combination of trend hunter and vwap mean reversion strategies that I published before.

Trend Hunter Strategy:

Mean Reversion Vwap Strategy:

The results are quite impressive, especially for bitcoin.

While the hodl return for bitcoin was 13419%, the strategy's return in the same period was about 5 times (65000%) of this.

s3.tradingview.com

In this combo strategy, I made some changes to the original settings of the strategies used together and added some more new features.

Trend Hunter Strategy Settings: (Original / Combo)

- Slow Tenkansen Period : 9 / 9

- Slow Kijunsen Period : 26 / 13

- Fast Tenkansen Period : 5 / 3

- Fast Kijunsen Period : 13 / 7

- BB Length : 20 / 20

- BB Stdev : 2 / 2

- TSV Length : 13 / 20

- TSV Ema Length : 7 / 7

* I also added a "vidya moving average" to be used as a confirmation tool to open a long position. (Candle close must be above the vidya line.)

Vwap Mean Reversion Strategy Settings: (Original / Combo)

- Small Vwap : 2 / 8

- Big Vwap : 5 / 10

- Percent Below to Buy : 3 / 2

- RSI Period : 2 / 2

- RSI Ema Period : 5 / 5

- Maximum RSI Level for Buy : 30

* I also added a "mean vwap line" to be used for exits in this part of the strategy. In the original version, when small vwap crossovers big vwap, we close the position, but in this strategy we will wait for the close above the mean vwap.

TIPS AND WARNINGS

1-) The standard settings of this combo strategy is designed and tested with daily timeframe. For lower timeframes, you should change the strategy settings and find the best value for yourself.

2-) Only the mean vwap line is displayed on the graph. For a detailed view, you can delete the "//" marks from the plot codes in the strategy code.

3-) This is a strategy for educational and experimental purposes. It cannot be considered as investment advice. You should be careful and make your own risk assessment when opening real market trades using this strategy.

________________________________________________________

Bu stratejide, daha önce yayınladığım trend avcısı ve vwap ortalamaya geri dönüş stratejilerinin bir kombinasyonunu kullandım.

Sonuçlar özellikle bitcoin için oldukça etkileyici.

Bitcoin için hodl getirisi %13419 iken, stratejinin aynı dönemdeki getirisi bunun yaklaşık 5 katı (%65000) idi.

Bu kombo stratejide, birlikte kullanılan stratejilerin orijinal ayarlarında bazı değişiklikler yaptım ve bazı yeni özellikler ekledim.

Trend Avcısı Strateji Ayarları: (Orijinal / Combo)

- Yavaş Tenkansen Periyodu : 9 / 9

- Yavaş Kijunsen Periyodu : 26 / 13

- Hızlı Tenkansen Periyodu : 5 / 3

- Hızlı Kijunsen Periyodu : 13 / 7

- BB Uzunluğu : 20 / 20

- BB Standart Sapması : 2 / 2

- TSV Uzunluğu : 13 / 20

- TSV Ema Uzunluğu : 7 / 7

* Ayrıca long pozisyon açmak için onay aracı olarak kullanılmak üzere "vidya hareketli ortalama" ekledim. (Mum kapanışı vidya çizgisinin üzerinde olmalıdır.)

Vwap Ortalamaya Dönüş Stratejisi Ayarları: (Orijinal / Combo)

- Küçük Vwap : 2 / 8

- Büyük Vwap : 5 / 10

- Alış İçin Gerekli Fark Oranı : 3 / 2

- RSI Periyodu : 2 / 2

- RSI Ema Periyodu: 5 / 5

- Alış için gerekli maksimum RSI seviyesi : 30

* Stratejinin bu bölümünde pozisyondan çıkışlar için kullanılacak bir "ortalama vwap çizgisi" de ekledim. Orijinal versiyonda, küçük vwap, büyük vwap'ı yukarı kestiğinde pozisyonu kapatıyoruz, ancak bu stratejide, ortalama vwap'ın üzerindeki kapanışı bekleyeceğiz.

İPUÇLARI VE UYARILAR

1-) Bu birleşik stratejinin standart ayarları, günlük zaman dilimi ile tasarlanmış ve test edilmiştir. Daha düşük zaman dilimleri için strateji ayarlarını değiştirmeli ve kendiniz için en iyi değeri bulmalısınız.

2-) Grafikte sadece ortalama vwap çizgisi görüntülenir. Ayrıntılı bir görünüm için strateji kodundaki "plot" ile başlayan satırlarda grafikte görünmesini istediğiniz özelliğin önündeki "//" işaretlerini silebilirsiniz.

3-) Eğitim ve deneysel amaçlı bir stratejidir. Yatırım tavsiyesi olarak değerlendirilemez. Bu stratejiyi kullanarak gerçek piyasa işlem açarken dikkatli olmalı ve kendi risk değerlendirmenizi yapmalısınız.

VIOP Scalping - OriginalVIOP Scalping – Original is a rule-based scalping strategy ported from an original C# logic set. It aims to trade only when trend direction, momentum, and trend strength align, then manages the position using fixed take-profit/stop-loss percentages with an optional trailing mechanism to protect gains during favorable moves.

This strategy is provided for educational and backtesting purposes only. It is not financial advice and does not guarantee profitability. Always test thoroughly before any live usage.

Core Concept

Follow the dominant WMA trend, confirm momentum with EMA separation, filter conditions with RSI + ADX, then exit using fixed TP/SL with trailing behavior after a defined profit threshold.

How the Strategy Works

Trend Direction is defined by WMA: above WMA = long bias, below WMA = short bias.

Momentum is measured via Fast EMA vs Slow EMA and the EMA difference.

Trend Strength is confirmed using ADX (must exceed a threshold).

RSI filters trades to avoid entering when momentum is likely overextended or weak.

A no-trade session blocks entries during a predefined time window (default 09:30–10:05).

Exit logic uses fixed percent TP/SL, with an optional trailing mechanism that activates after a profit threshold.

Inputs and Settings

Trend and Indicator Settings

Main Trend WMA: Determines directional bias (price above = long, price below = short).

Fast EMA / Slow EMA: Used to measure momentum and directional separation.

RSI Period: Filters entries based on RSI range constraints.

ADX Period: Measures trend strength (must exceed threshold to allow entries).

Threshold Settings

EMA Difference Threshold: Minimum EMA separation required to validate momentum.

ADX Threshold: Minimum ADX required to confirm trend strength.

RSI Long Ceiling: RSI must remain below this value for long entries.

RSI Short Floor: RSI must remain above this value for short entries.

Risk Management Settings

Take Profit %: Default TP distance in percent.

Strong Trend Take Profit %: Higher TP used when a “strong trend” condition is detected.

Stop Loss %: Fixed SL distance in percent.

Trailing Activation %: Profit threshold at which trailing starts.

Trailing Distance %: Trailing offset distance used once trailing is active.

Time Filter

No-Trade Hours: Default session is 09:30–10:05. During this window, the strategy does not open new trades.

Entry Logic

No-Trade Time Filter

If the current bar falls inside the no-trade session, entries are blocked.

Long Entry Conditions

Price is above the WMA trend line.

EMA difference is positive and greater than the EMA Difference Threshold.

EMA momentum is increasing (current EMA diff > previous EMA diff).

RSI is within the defined range (RSI > 48 and RSI < RSI Long Ceiling).

Close is higher than the previous close.

ADX is above the ADX Threshold.

Short Entry Conditions

Price is below the WMA trend line.

EMA difference is negative and lower than -EMA Difference Threshold.

Bearish momentum is increasing (current EMA diff < previous EMA diff).

RSI is within the defined range (RSI < 52 and RSI > RSI Short Floor).

Close is lower than the previous close.

ADX is above the ADX Threshold.

Strong Trend Logic (Dynamic TP Selection)

If price is far from the WMA (absolute distance > 20 points) AND EMA separation is strong (absolute EMA diff > 1.5 points), the strategy treats the environment as a strong trend.

In strong trend mode, the strategy uses “Strong Trend Take Profit %” instead of the default “Take Profit %”.

Exit Management (TP/SL + Trailing)

The strategy uses fixed percentage-based TP and SL levels.

Trailing logic is enabled via strategy.exit and activates only after price moves in profit by the defined Trailing Activation %.

Once activated, trailing follows price using the defined Trailing Distance % offset.

This is designed to secure partial gains during extended moves while still allowing room for continuation.

What You See on the Chart

WMA Trend Line (Main Trend Filter).

Fast EMA and Slow EMA (Momentum Confirmation).

Strategy entry/exit markers generated by TradingView.

Recommended Use

Scalping systems that rely on trend-following and momentum confirmation.

Markets where ADX filtering helps avoid choppy conditions.

Traders who want a simple, parameter-driven TP/SL system with trailing after confirmation.

Important Notes

The no-trade session depends on your chart/session settings. Ensure your symbol/session configuration matches your intended market hours.

Percent-based exits scale with price; results will vary across instruments and volatility regimes.

Always validate behavior using bar replay, forward testing, and realistic commission/slippage assumptions.

Systematic Investment Tracker by Ceyhun Gonul### English Description

**Systematic Investment Tracker with Enhanced Features**

This script, titled **Systematic Investment Tracker with Enhanced Features**, is a TradingView tool designed to support systematic investments across different market conditions. It provides traders with two customizable investment strategies — **Continuous Buying** and **Declining Buying** — and includes advanced dynamic investment adjustment features for each.

#### Detailed Explanation of Script Features and Originality

1. **Two Investment Strategies**:

- **Continuous Buying**: This strategy performs purchases consistently at each interval, as set by the user, regardless of market price changes. It follows the principle of dollar-cost averaging, allowing users to build an investment position over time.

- **Declining Buying**: Unlike Continuous Buying, this strategy triggers purchases only when the asset's price has declined from the previous interval's closing price. This approach helps users capitalize on lower price points, potentially improving average costs during downward trends.

2. **Dynamic Investment Adjustment**:

- For both strategies, the script includes a **Dynamic Investment Adjustment** feature. If enabled, this feature increases the purchasing amount by 50% if the current price has fallen by a specific user-defined percentage relative to the previous price. This allows users to accumulate a larger position when the asset is declining, which may benefit long-term cost-averaging strategies.

3. **Customizable Time Frames**:

- Users can specify a **start and end date** for investment, allowing them to restrict or backtest strategies within a specific timeframe. This feature is valuable for evaluating strategy performance over specific market cycles or historical periods.

4. **Graphical Indicators and Labels**:

- The script provides graphical labels on the chart that display purchase points. These indicators help users visualize their investment entries based on the strategy selected.

- A summary **performance label** is also displayed, providing real-time updates on the total amount spent, accumulated quantity, average cost, portfolio value, and profit percentage for each strategy.

5. **Language Support**:

- The script includes English and Turkish language options. Users can toggle between these languages, allowing the summary label text and descriptions to be displayed in their preferred language.

6. **Performance Comparison Table**:

- An optional **Performance Comparison Table** is available, offering a side-by-side analysis of net profit, total investment, and profit percentage for both strategies. This comparison table helps users assess which strategy has yielded better returns, providing clarity on each approach's effectiveness under the chosen parameters.

#### How the Script Works and Its Uniqueness

This closed-source script brings together two established investment strategies in a single, dynamic tool. By integrating continuous and declining purchase strategies with advanced settings for dynamic investment adjustment, the script offers a powerful, flexible tool for both passive and active investors. The design of this script provides unique benefits:

- Enables automated, systematic investment tracking, allowing users to build positions gradually.

- Empowers users to leverage declines through dynamic adjustments to optimize average cost over time.

- Presents an easy-to-read performance label and table, enabling an efficient and transparent performance comparison for informed decision-making.

---

### Türkçe Açıklama

**Gelişmiş Özellikli Sistematik Yatırım Takipçisi**

**Gelişmiş Özellikli Sistematik Yatırım Takipçisi** adlı bu TradingView scripti, çeşitli piyasa koşullarında sistematik yatırım stratejilerini desteklemek üzere tasarlanmış bir araçtır. Script, kullanıcıya iki özelleştirilebilir yatırım stratejisi — **Sürekli Alım** ve **Düşen Alım** — ve her strateji için gelişmiş dinamik yatırım ayarlama seçenekleri sunar.

#### Script Özelliklerinin Detaylı Açıklaması ve Özgünlük

1. **İki Yatırım Stratejisi**:

- **Sürekli Alım**: Bu strateji, fiyat değişimlerine bakılmaksızın kullanıcının belirlediği her aralıkta sabit bir miktar yatırım yapar. Bu yaklaşım, uzun vadede pozisyonu kademeli olarak oluşturmak isteyenler için idealdir.

- **Düşen Alım**: Sürekli Alım’ın aksine, bu strateji yalnızca fiyat bir önceki aralığın kapanış fiyatına göre düştüğünde alım yapar. Bu yöntem, yatırımcıların daha düşük fiyatlardan alım yaparak ortalama maliyeti potansiyel olarak iyileştirmelerine yardımcı olur.

2. **Dinamik Yatırım Ayarlaması**:

- Her iki strateji için de **Dinamik Yatırım Ayarlaması** özelliği bulunmaktadır. Bu özellik aktif edildiğinde, mevcut fiyatın bir önceki fiyata göre kullanıcı tarafından belirlenen bir yüzde oranında düşmesi durumunda alım miktarını %50 artırır. Bu durum, uzun vadede maliyet ortalaması stratejilerine katkıda bulunur.

3. **Özelleştirilebilir Tarih Aralığı**:

- Kullanıcılar, yatırımı belirli bir tarih aralığında sınırlandırmak veya test etmek için bir **başlangıç ve bitiş tarihi** belirleyebilir. Bu özellik, strateji performansını geçmiş piyasa döngüleri veya belirli dönemlerde değerlendirmek için kullanışlıdır.

4. **Grafiksel İşaretleyiciler ve Etiketler**:

- Script, grafik üzerinde alım noktalarını gösteren işaretleyiciler sağlar. Bu görsel göstergeler, kullanıcıların seçilen stratejiye göre yatırım girişlerini görselleştirmesine yardımcı olur.

- Ayrıca, her strateji için harcanan toplam tutar, biriken miktar, ortalama maliyet, portföy değeri ve kâr yüzdesi gibi bilgileri gerçek zamanlı olarak gösteren bir **performans etiketi** sunar.

5. **Dil Desteği**:

- Script, İngilizce ve Türkçe dillerini desteklemektedir. Kullanıcılar, performans etiketi metninin ve açıklamalarının tercih ettikleri dilde görüntülenmesi için dil seçimini yapabilir.

6. **Performans Karşılaştırma Tablosu**:

- İsteğe bağlı olarak kullanılabilen bir **Performans Karşılaştırma Tablosu**, her iki strateji için net kâr, toplam yatırım ve kâr yüzdesi gibi bilgileri yan yana analiz eder. Bu tablo, kullanıcıların hangi stratejinin daha yüksek getiri sağladığını değerlendirmesine yardımcı olur.

#### Scriptin Çalışma Prensibi ve Özgünlüğü

Bu script, iki yatırım stratejisini gelişmiş bir araçta birleştirir. Sürekli ve düşen fiyatlara dayalı alım stratejilerini dinamik yatırım ayarlama özelliğiyle entegre ederek yatırımcılar için güçlü ve esnek bir çözüm sunar. Script’in tasarımı aşağıdaki benzersiz faydaları sağlamaktadır:

- Otomatik, sistematik yatırım takibi yaparak kullanıcıların pozisyonlarını kademeli olarak oluşturmalarına olanak tanır.

- Dinamik ayarlama ile düşüşlerden yararlanarak zaman içinde ortalama maliyeti optimize etme olanağı sağlar.

- Her iki stratejinin performansını basit ve anlaşılır bir şekilde karşılaştıran etiket ve tablo ile verimli bir performans değerlendirmesi sunar.

SPX Iron Fly Session TrackerOverview

This indicator provides visual tracking for iron fly option structures designed for SPX 0-day-to-expiration (0DTE) intraday trading. It implements a two-phase position management system that adapts to different market conditions throughout the trading day.

This is a visualization and tracking tool only. It does not execute trades, access real options data, or calculate actual profit and loss. All displayed positions are theoretical representations based on underlying price movement.

Strategy Goal and Context

The Core Objective:

The strategy aims to have SPX price expire within your iron fly positions at end of day. When price expires inside a fly's profit zone (between the wings), that position captures maximum premium. The challenge is that price moves throughout the day, so static positioning rarely succeeds.

The Solution: Active Management

Rather than setting positions and hoping price cooperates, this approach continuously manages and repositions flies to keep price centered within your profit zones. As SPX drifts during the trading session, you add new flies at current price levels and close flies that price has moved away from.

The Goal: Multiple Profitable Expirations

By session end, you want as many flies as possible to have price expire within their center zones. This requires:

Adding new flies as price moves away from existing positions

Closing flies when price crosses beyond their optimal range

Building layered coverage in the afternoon to increase probability of capture

Adapting wing widths to time of day and volatility

The Reality: Capital and Time Intensive

This is not a passive strategy. Successful implementation requires:

Substantial capital (each fly requires margin, multiple flies compound this)

Active monitoring throughout trading sessions

Quick decision-making as positions trigger

Multiple position adjustments per session

Disciplined adherence to management rules

How This Indicator Helps:

For backtesting:

Use replay mode to study how positions would have managed on historical sessions

Test different parameter combinations to find optimal settings

Observe position behavior during various market conditions

Understand timing and frequency of position adds and closes

Validate whether your capital can support the required position count

For live session support:

Real-time visual tracking shows current position coverage

Alerts notify you immediately when new positions should be added

Position closure alerts help you manage exits promptly

Reference strike tracking shows where you're measuring movement from

History table provides audit trail of all position activity

The indicator handles the complex tracking and rule application, allowing you to focus on execution and risk management.

Key Use Cases

1. Replay Mode - Backtest and Study

Use TradingView's replay feature to validate the strategy on historical sessions:

Step through past SPX sessions bar-by-bar

See exactly when positions would have opened and closed

Count how many flies would have expired profitably

Analyze different parameter settings on the same historical data

Study position behavior during trending vs ranging conditions

Calculate approximate capital requirements for your setup

Refine your parameters before risking real capital

2. Live Session Alerts

Set up real-time notifications for active trading sessions:

Get alerted immediately when new positions trigger

Receive notifications when positions close

Alerts include strike level, wing width, and closure reason

Works on mobile, desktop, email, or webhook

Never miss a position signal during active trading

Maintain awareness even when away from screens briefly

3. Fully Customizable Parameters

Adapt every aspect to your risk tolerance and capital:

Adjust trigger distances for more or fewer position adds

Modify wing widths for different volatility environments

Change session timing to match your trading schedule

Set maximum concurrent positions to your capital limits

Fine-tune spacing to match available strike increments

Iron Fly Structure

An iron fly is a neutral options strategy with four legs:

- Short 1 ATM Call

- Short 1 ATM Put

- Long 1 OTM Call (upper wing protection)

- Long 1 OTM Put (lower wing protection)

The structure creates a defined risk zone. Maximum profit occurs when price expires at the center strike. Loss increases as price moves toward the wings (breakeven points). Maximum loss is defined and occurs beyond the wings.

Expiration Goal:

You want SPX to close inside the fly's wings. If SPX expires at the strike, you capture maximum premium. If SPX expires between the strike and either wing, you still profit (reduced). If SPX expires beyond the wings, you realize a loss (but it's defined and limited by the wings).

Two-Phase Management System

The indicator tracks positions across two distinct trading phases with different management rules:

Phase 1: TWO_GLASS - Morning Session (Default 10am-1pm ET)

Conservative positioning with active repositioning:

- Trigger new positions when price moves 7.5 points from reference strike (configurable)

- Maintain maximum 2 concurrent positions (configurable)

- 10-point spacing between position strikes (configurable)

- 40-point wing width (configurable)

- Exit rule: When two positions are active and price crosses to one strike level, close the OTHER position

This phase uses a "follow the price" approach. You're not trying to stack multiple positions yet - you're maintaining one or two flies centered on wherever price currently is. As price drifts, you add a new fly at the current level and close the old one when price moves too far away.

Phase 2: THREE_GLASS - Afternoon Session (Default 1pm-4pm ET)

Accumulation mode with layered coverage:

- Trigger new positions every 2.5 points of price movement (configurable)

- Maintain maximum 6 concurrent positions (configurable)

- 5-point spacing between strikes (configurable)

- 20-point wings early, reducing to 10 points after 3pm (configurable)

- Exit rule: Positions only close when price reaches wing extremes

This phase builds a stacked profit zone. Instead of swapping positions, you accumulate multiple flies as price moves. The goal is to have several flies active at expiration, creating a wider net to capture price. Tighter spacing and more frequent triggers create this layered coverage.

Why Two Different Phases?

Morning (Phase 1):

Earlier in the day, price has more time to move substantially. Maintaining many concurrent positions is riskier because price could trend and hit multiple wings. The strategy uses selective positioning with wider wings and active replacement.

Afternoon (Phase 2):

Closer to expiration, price movements typically compress. Time for large moves decreases. The strategy shifts to accumulation, building a net of positions to increase probability that final expiration price falls within at least one (ideally several) of your flies. Tighter wings and more positions become appropriate.

Exit Mechanisms

Strike Cross Exit (Phase 1 Only)

When two positions are active, if price moves to or beyond one position's strike level, the OTHER position closes. This keeps your coverage centered on current price action rather than maintaining positions price has moved away from.

Example: Flies at 5900 and 5910 are open. Price moves to 5910. The fly at 5900 closes because price has moved to the 5910 level. You're now positioned at current price (5910) rather than maintaining coverage at old price (5900).

Wing Extreme Exit (Both Phases)

Any position closes immediately when price touches its upper or lower wing boundary. This represents the breakeven/maximum loss point, so the position is closed to prevent further deterioration.

Dynamic Wing Adjustment

Wing widths automatically adjust based on time of day:

- Phase 1 (Morning): 40 points (customizable)

- Phase 2 Early (1pm-3pm): 20 points (customizable)

- Phase 2 Late (3pm-4pm): 10 points (customizable)

This progressive tightening reflects decreasing price movement potential as expiration approaches. Wider wings earlier provide more protection when price could move substantially. Tighter wings later allow more precise positioning when price movements typically compress.

All values are fully adjustable to match your risk parameters and observed market volatility.

Customization Guide

Every parameter can be modified to suit your trading style, risk tolerance, and capital:

Session Timing

- TWO_GLASS Start Hour: When Phase 1 begins (default: 10am ET)

- THREE_GLASS Start Hour: When Phase 2 begins (default: 1pm ET)

- Wing Width Change Hour: When wings tighten (default: 3pm ET)

- Session End Hour: When tracking stops (default: 4pm ET)

Phase 1 Parameters (Fully Adjustable)

- Trigger Distance: How far price must move from reference strike to add new position (default: 7.5, range: 0.1+)

- Fly Spacing: Distance between position strikes (default: 10, range: 1.0+)

- Wing Width: Distance from strike to wings (default: 40, range: 5.0+)

- Max Flies: Maximum concurrent positions (default: 2, range: 1-10)

Phase 2 Early Parameters (Fully Adjustable)

- Trigger Distance: Movement needed to add new position (default: 2.5, range: 0.1+)

- Fly Spacing: Distance between strikes (default: 5, range: 1.0+)

- Wing Width: Strike to wing distance (default: 20, range: 5.0+)

- Max Flies: Maximum concurrent positions (default: 6, range: 1-20)

Phase 2 Late Parameters

- Wing Width: Reduced width after 3pm (default: 10, range: 5.0+)

General Settings

- Strike Rounding: Round strikes to nearest multiple (default: 5.0, range: 1.0+)

- Bars Before Check: Bars to wait before allowing closure (default: 2, prevents premature exits)

Display Options

- Show History Table: Toggle detailed position log (default: on)

- History Table Rows: Number of positions displayed (default: 15, range: 5-30)

Alert Settings

- Enable Alerts: Toggle notifications for opens/closes (default: on)

How to Use

For Backtesting in Replay Mode:

Select a historical SPX trading session

Apply indicator to 1-5 minute timeframe

Configure your preferred parameters

Activate TradingView's replay feature

Play through the session (step-by-step or continuous)

Observe when positions open (green boxes appear)

Watch position closures (boxes turn gray)

Count how many flies would have expired with price inside (green at session end)

Note total number of position adds throughout session

Calculate approximate capital needed (positions × margin per fly)

Test different parameter combinations on same historical data

Study position behavior during trending vs ranging sessions

For Live Trading Sessions:

Apply indicator to SPX on 1-5 minute timeframe

Configure parameters based on your backtest results

Create alerts for "Iron Fly Opened" and "Iron Fly Closed"

Set alert frequency to "Once Per Bar Close"

Choose notification method (popup, mobile app, email, webhook)

Monitor the status table (top-right) for current session and reference strike

Review history table (bottom-right) for position log with timestamps

When alert triggers, use visual cues to manually place actual option orders

Execute position adds and closes as indicated by the tracker

Visual Interpretation:

Green boxes = Active positions (theoretical profit zones)

White lines (Phase 1) / Aqua lines (Phase 2) = Strike levels

Red/Blue dotted lines = Wing boundaries (breakeven/risk limits)

Gray boxes = Closed positions (historical reference)

Current SPX price line = Shows where price is relative to positions

Top-right table = Current session status, reference strike, open/closed counts

Bottom-right table = Complete position history with open/close timestamps

Alert System Details

The indicator generates detailed alert messages for position management:

Position Opened:

- Strike level where fly should be placed

- Wing width (±points from strike)

- Session phase (Phase 1 or Phase 2)

- Alert format example: "Iron Fly OPENED | Strike: 5900 | Wings: ±40 | Session: TWO_GLASS"

Position Closed:

- Strike level of fly being closed

- Closure reason (strike cross, wing extreme, etc.)

- Session phase

- Alert format example: "Iron Fly CLOSED | Strike: 5900 | Reason: Price crossed to lower fly | Session: TWO_GLASS"

Configure alerts once before market open, then receive automatic notifications as positions trigger throughout the trading session.

Parameter Optimization Suggestions

For Higher Volatility Environments:

- Increase trigger distances (e.g., Phase 1: 10-15 points, Phase 2: 3-5 points)

- Widen wing widths (e.g., Phase 1: 50-60 points, Phase 2: 25-30 points early, 15-20 late)

- Increase strike spacing to reduce position frequency

For Lower Volatility Environments:

- Decrease trigger distances (e.g., Phase 1: 5-7 points, Phase 2: 1.5-2 points)

- Tighten wing widths (e.g., Phase 1: 30-35 points, Phase 2: 15-18 points early, 8-10 late)

- Reduce strike spacing for more granular coverage

For Conservative Risk Management:

- Reduce maximum concurrent positions (Phase 1: 1, Phase 2: 3-4)

- Widen wing widths for more breathing room

- Increase bars before check to avoid whipsaws

- Use wider trigger distances to reduce position frequency

For Aggressive Positioning:

- Increase maximum concurrent positions (Phase 2: 8-10)

- Tighten trigger distances for more frequent adds

- Reduce bars before check for faster responses

- Use tighter spacing to create denser coverage

Capital Considerations:

Remember that each fly requires margin. If Phase 2 allows 6 concurrent flies and each requires $10,000 margin, you need $60,000 in available capital just for position requirements, plus additional cushion for adverse movement.

Use replay mode to count maximum concurrent positions that would have occurred on historical sessions with your parameters, then calculate total capital needed.

Practical Application

This tool provides visual guidance and management support. To implement the strategy:

Backtest thoroughly in replay mode first

Validate capital requirements for your parameter settings

Confirm you can actively monitor positions during trading hours

Use displayed positions as reference for manual order placement

Match indicator parameters to your actual option contracts

Account for real-world factors: commissions, slippage, bid-ask spreads, option availability

Implement proper position sizing based on available capital

Set up alerts before market open to catch all signals

Execute actual trades manually in your brokerage platform

Track actual results versus indicator expectations

Important Limitations

Theoretical tracking only - not an automated trading system

No access to real option prices, Greeks, or implied volatility

No profit/loss calculations or risk metrics

Does not account for time decay (theta), delta, gamma, vega changes

Assumes continuous price action - gaps or halts not handled

Designed for 0DTE SPX options - not suitable for other timeframes or instruments

Assumes option availability at all strike levels - may not reflect reality

Does not model actual option bid/ask spreads or liquidity

Assumes instant execution at desired strikes - slippage not considered

Historical replay shows theoretical behavior only - actual market conditions may differ

Does not adjust for changing implied volatility throughout session

Position count and timing may not match what's executable in real markets

Capital and Time Requirements

This strategy is resource-intensive:

Capital Requirements:

Each iron fly requires margin (varies by broker and strike width)

Multiple concurrent positions multiply capital needs

Example: 6 flies at $10,000 each = $60,000 minimum

Additional cushion needed for adverse movement

Pattern Day Trader rules may apply (requires $25,000 minimum)

Time Requirements:

Active monitoring during trading hours (typically 10am-4pm ET)

Quick response to position add/close signals

Multiple position adjustments per session possible

Cannot be passive or set-and-forget

Requires ability to place orders promptly when alerted

Use replay mode to understand the commitment level before attempting live implementation.

Risk Considerations

Iron fly trading involves substantial risk. This indicator provides visualization and management support only - it does not constitute financial advice or trading recommendations.

Options trading can result in total loss of capital. The indicator's theoretical positions do not reflect actual trading results. Backtest analysis and historical visualization do not guarantee similar future outcomes. Multiple concurrent positions multiply both profit potential and loss risk.

Always conduct independent research, understand all risks, validate capital requirements, and never trade with funds you cannot afford to lose. Consider starting with paper trading to validate execution capability before risking real capital.

Technical Notes

The indicator uses price-based triggers only. It does not:

Connect to options data feeds

Calculate theoretical option values or Greeks

Execute trades automatically

Provide specific trading signals or recommendations

Account for option-specific factors (implied volatility, time decay, bid/ask spreads)

All displayed information represents theoretical position placement based solely on underlying SPX price movement and user-configured parameters. The tool helps visualize the management framework but requires the trader to handle all actual execution and risk management decisions.

This is an educational and analytical tool for understanding iron fly position management concepts. It requires active interpretation, backtesting validation, and manual implementation by the user.